How I Navigated Contract Disputes with Smart Financial Tools—And What Worked

Contract disputes can hit anyone—freelancers, small businesses, even gig workers. I learned this the hard way when a deal went south and left me scrambling. What saved me wasn’t luck, but the right financial tools used at the right time. In this article, I’ll walk you through the practical strategies that helped me protect my income, reduce risk, and stay in control when legal tensions rose. These aren’t theoretical ideas—they’re real, tested approaches that brought clarity and stability during a stressful time. Whether you’re managing client projects or running a home-based business, understanding how to use financial tools wisely can make the difference between financial strain and lasting security.

When Contracts Go Wrong: A Common Financial Blind Spot

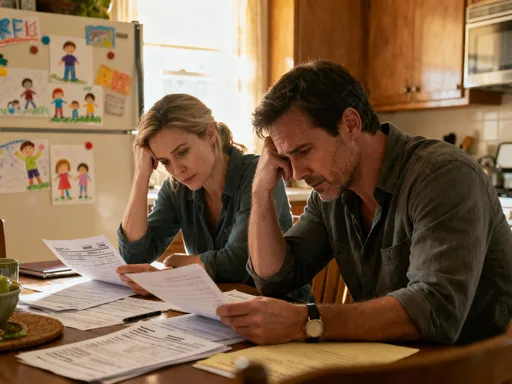

It starts innocently enough—a handshake agreement, a quick email confirming terms, or a simple contract missing key details. Many people operate under the assumption that professionalism and mutual respect will carry a project to completion. But in reality, even well-intentioned partnerships can unravel. Misunderstandings about deliverables, delayed payments, or sudden project cancellations are more common than most realize, especially among independent professionals and small business owners. These situations aren’t always signs of bad faith; sometimes, they stem from unclear expectations, shifting priorities, or simple miscommunication. Yet, the financial consequences can be severe, particularly for those without a buffer or backup income.

The truth is, every contract carries an element of risk, and failing to prepare for potential disputes is a financial blind spot that can lead to lost income, damaged credit, or even legal fees. For individuals managing household budgets or relying on side income to support family needs, such setbacks can ripple into daily life—delaying bill payments, increasing stress, or forcing difficult choices about spending. The problem is often not the dispute itself, but the lack of systems in place to manage it. Relying solely on verbal promises or informal arrangements leaves little recourse when things go wrong. Without documented terms and financial safeguards, proving your case becomes difficult, and collecting what you’re owed can feel impossible.

One of the most common triggers is ambiguous payment terms. For example, a client may agree to pay “upon completion,” but what counts as completion? Without clearly defined milestones or acceptance criteria, both parties may have different interpretations. Similarly, vague timelines or missing clauses about revisions and scope changes open the door to disagreements. Even a seemingly minor oversight, like failing to specify currency or late fees, can escalate into a larger conflict. These gaps don’t just create confusion—they create financial exposure. And when income is tied to a single project or client, that exposure can become a crisis. The lesson here is not to assume good intentions will be enough. Instead, it’s essential to treat every agreement as a financial instrument that needs structure, clarity, and protection.

The Role of Financial Tools in Dispute Prevention

Prevention is always more effective—and less costly—than resolution. The most powerful way to avoid contract disputes is not through legal threats, but through clear, consistent financial practices supported by the right tools. Modern financial technology offers practical solutions that help both parties stay aligned from the start. One of the most effective strategies is milestone-based invoicing. Instead of waiting for a project to end before requesting payment, breaking the work into phases with associated payments ensures steady cash flow and provides built-in checkpoints. Each milestone acts as a mini-agreement, confirming that a portion of the work has been accepted before moving forward. This approach reduces the risk of non-payment and gives both sides a shared timeline to follow.

Digital payment trackers are another valuable asset. These tools automatically log when invoices are sent, viewed, and paid, creating a neutral, time-stamped record of financial interactions. Unlike email chains or paper receipts, which can be lost or disputed, digital trackers provide verifiable data that both parties can access. When a client claims they never received an invoice, a simple screenshot from the tracker can resolve the issue instantly. Similarly, automated reminders reduce the awkwardness of chasing payments while keeping the process professional. These reminders can be scheduled to go out a few days before a due date and again after it passes, maintaining momentum without constant manual follow-up.

These tools do more than improve efficiency—they build accountability. When payment terms are linked directly to deliverables and tracked in real time, there’s less room for misunderstanding. If a dispute arises, the financial record becomes evidence of what was agreed upon and when. This is especially important for individuals who may not have the resources to hire legal counsel. By using financial tools proactively, you create a system that protects your interests without requiring confrontation. The goal isn’t to distrust your clients, but to ensure that trust is supported by structure. In this way, financial tools become not just administrative aids, but essential components of risk management.

Choosing the Right Platforms: Integration and Transparency

Not all financial platforms are created equal, and choosing the wrong one can leave you vulnerable when a dispute arises. The key is to select tools that prioritize transparency, offer strong audit trails, and integrate smoothly with your existing systems. Accounting software, for example, goes beyond basic bookkeeping by allowing you to attach contracts, track project income, and generate detailed reports. Look for platforms that automatically timestamp every transaction and maintain a version history of documents. This ensures that if a client later denies agreeing to certain terms, you can produce a record showing exactly when and how the agreement was made.

Escrow services are another option worth considering, especially for larger projects or new client relationships. These services hold payments in a secure account until both parties confirm that the work is complete. This protects the service provider from non-payment and gives the client assurance that funds won’t be released until expectations are met. While escrow may involve a small fee, the peace of mind—and financial protection—it offers can be well worth the cost. For many freelancers and small business owners, this added layer of security makes high-value contracts feel less risky.

Contract management apps also play a crucial role. These tools combine document storage with payment tracking and deadline alerts, creating a centralized hub for all project-related information. Some even allow both parties to sign agreements electronically, with digital signatures that carry legal weight in many jurisdictions. When evaluating platforms, consider how easily they connect with your bank, payment processors, and email. Seamless integration means less manual data entry and fewer opportunities for errors. It also means you can generate comprehensive reports quickly if a dispute escalates. The best platforms don’t just store information—they make it actionable, giving you the ability to respond swiftly and confidently when challenges arise.

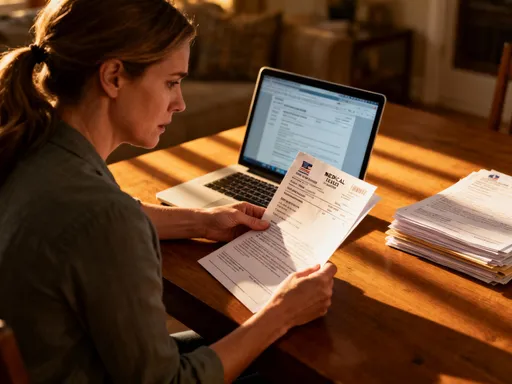

Documenting Every Move: Building a Financial Paper Trail

In any contract dispute, your strongest defense is documentation. A well-organized financial paper trail doesn’t just support your position—it can prevent a conflict from escalating in the first place. The idea isn’t to become a legal archivist, but to adopt simple, consistent habits that keep important records accessible. Start by saving every communication related to the project: emails, text messages, video call summaries, and change requests. Store these in a dedicated folder, either in the cloud or on a secure drive, labeled clearly with the client name and date. Treat every message as potential evidence, even if it seems minor at the time.

Invoices and receipts should be saved in both digital and, if necessary, printed form. Use a naming convention that makes files easy to find—such as “ClientName_Invoice_042524”—and include key details like project scope, payment terms, and due dates. When a client requests changes, send a revised invoice or agreement outlining the new terms and get confirmation before proceeding. This prevents “scope creep,” where additional work is expected without additional pay. If a client agrees verbally, follow up with an email summarizing the change and ask for confirmation. This creates a written record of consent, which can be critical later.

Project updates should also be documented regularly. Whether you’re a graphic designer, consultant, or home renovation contractor, sending weekly progress reports with photos, drafts, or completed tasks keeps the client informed and creates a timeline of your work. These updates serve a dual purpose: they build trust during the project and provide proof of completion if payment is delayed. If a dispute arises, you can point to a clear sequence of deliverables and approvals. The goal is to make your case so well-documented that resolution becomes a matter of reviewing facts, not arguing opinions. Over time, this practice becomes second nature, reducing stress and increasing confidence in every client relationship.

Managing Cash Flow Amid Legal Uncertainty

One of the most stressful aspects of a contract dispute is the impact on cash flow. When a payment is delayed or withheld, it can disrupt your ability to cover personal or business expenses. For families relying on this income, the consequences can be immediate—delayed rent, missed utility payments, or difficulty buying groceries. The key to navigating this challenge is preparation. Building a financial buffer specifically for contractual conflicts can provide critical breathing room. This doesn’t mean saving thousands overnight, but setting aside a portion of each payment into a separate emergency fund. Even a few hundred dollars can make a difference when a client delays payment for weeks.

Diversifying your income sources is another effective strategy. Relying on a single client or project increases your vulnerability. By working with multiple clients or offering different services, you reduce the impact of any one dispute. This doesn’t mean overextending yourself, but rather creating a more resilient financial structure. If one income stream is interrupted, others can help maintain stability. Additionally, consider using a line of credit or short-term loan as a temporary bridge, but only if the interest rate is manageable and repayment is certain. These tools should be used cautiously, not as a long-term solution, but as a way to avoid financial strain during uncertain periods.

It’s also important to adjust your financial forecasts when a dispute arises. If a payment is in question, don’t count it as income until it’s in your account. Update your budget to reflect the uncertainty and prioritize essential expenses. Avoid the temptation to spend money you expect to receive, as this can lead to further stress if the payment doesn’t come through. Emotional spending—such as making unplanned purchases to cope with stress—should also be avoided. Instead, focus on maintaining control through disciplined financial habits. By treating cash flow management as an ongoing practice, you build resilience that protects not just your business, but your household’s financial well-being.

Knowing When to Escalate—and When to Walk Away

Even with the best tools and documentation, some disputes cannot be resolved through communication alone. At a certain point, you must decide whether to escalate the matter or accept the loss and move on. This decision should not be based on emotion, but on a clear assessment of costs, time, and long-term impact. Escalation options include mediation, arbitration, or small claims court, each with its own financial and emotional toll. Mediation involves a neutral third party helping both sides reach an agreement and is often less expensive than formal legal action. Arbitration is more structured and binding but can still be costly. Small claims court is accessible and designed for individuals without legal representation, but it requires time and preparation.

Before choosing any of these paths, calculate the total value of the disputed amount against the potential costs. If the fee for filing a claim is $100 and the amount owed is $300, the math may still favor action. But if the process will take months and require significant effort, the emotional and opportunity cost may outweigh the benefit. Consider also the impact on your reputation and future business. While standing up for your rights is important, prolonged conflict can drain your energy and affect your relationships with other clients. In some cases, writing off a small amount may be the most practical choice, especially if the client is unlikely to pay regardless of the outcome.

There’s no shame in walking away when the cost of fighting exceeds the reward. The real victory lies in what you learn and how you improve your systems moving forward. Every dispute, resolved or not, offers insight into where your processes can be strengthened. The goal is not to win every battle, but to build a business that is less vulnerable to future conflicts. By setting clear financial benchmarks for when to escalate—such as a minimum dollar threshold or evidence of repeated non-payment—you create a rational framework for decision-making. This removes emotion from the process and helps you act with clarity and confidence.

Lessons Learned: Building a Resilient Financial Routine

The experience of navigating a contract dispute taught me that financial security isn’t just about earning income—it’s about protecting it. The tools and habits I adopted didn’t just help me through one crisis; they became part of a broader, more resilient financial routine. Today, I use standardized contract templates for every project, clearly outlining payment terms, deliverables, deadlines, and revision policies. Before work begins, I conduct a brief pre-contract check-in to confirm expectations with the client. This simple step prevents misunderstandings and builds mutual accountability from the start.

I also schedule regular financial reviews—monthly or quarterly—to assess my income streams, outstanding payments, and emergency reserves. This helps me identify potential risks early and adjust my plans as needed. I’ve integrated digital tools into my daily workflow, so documentation and tracking happen automatically, not as an afterthought. Over time, these practices have reduced my stress and increased my confidence in every client relationship. I no longer fear disputes because I know I’m prepared.

For anyone managing income—whether from a side hustle, freelance work, or a small business—these lessons are within reach. You don’t need a law degree or a large budget to protect yourself. What matters is consistency, clarity, and the willingness to treat financial safety as an ongoing priority. By embedding dispute-ready habits into your routine, you build a foundation that supports not just your business, but your family’s long-term stability. Financial resilience isn’t built in a day, but through small, deliberate actions that add up over time. And when challenges arise, you’ll be ready—not because of luck, but because you’ve put the right systems in place.