How I Smartly Funded My Kid’s Study Tour Without Stress

Sending your child on a study tour is exciting—but the cost? Not so much. I was overwhelmed too, until I discovered simple investment tools that actually work. No get-rich-quick schemes, just practical strategies that grow money over time. This is how I turned monthly savings into a fully funded trip, without dipping into emergency funds or racking up debt. If you're worried about education expenses, this approach might be the game-changer you need. What started as a quiet concern about affordability became a journey of financial clarity and confidence. The key wasn’t earning more—it was using what I already had, more wisely.

The Real Cost of Study Tours—And Why Savings Aren’t Enough

Study tours are more than just trips; they are immersive learning experiences that combine travel with academic growth. Whether it’s a two-week cultural exchange in Europe or a science-focused field trip in North America, these programs offer students real-world exposure that classrooms alone cannot provide. However, the benefits come with a price tag that often surprises parents. On average, a reputable international study tour can cost between $3,000 and $7,000, depending on destination, duration, and inclusions such as flights, accommodation, meals, and guided activities. Even domestic or regional programs can range from $800 to $2,500. These figures do not include extras like travel insurance, visas, pocket money, or personal shopping—costs that can add hundreds more to the total.

Many families begin planning with good intentions, setting aside a fixed amount each month in a regular savings account. While this shows discipline, it may not be enough to meet the full cost when the time comes. The reason lies in inflation and the slow pace of traditional savings growth. Over a two- or three-year period, inflation can erode the real value of saved money by 5% to 10%, depending on economic conditions. At the same time, study tour fees often rise year after year due to increasing operational costs, currency fluctuations, and demand. A program that costs $4,500 today might cost $5,000 or more just two years later. If your savings account earns only 0.5% to 1% annual interest, you’re effectively losing ground.

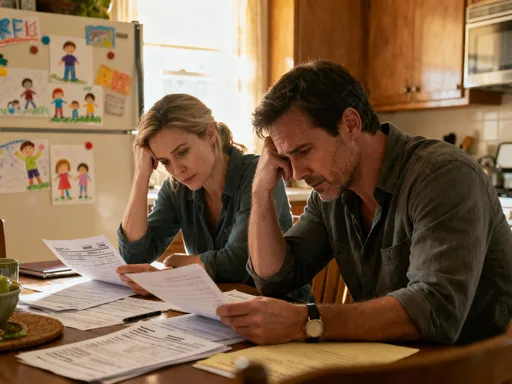

Beyond the numbers, there’s an emotional dimension to this challenge. Parents want to support their children’s growth, but the financial pressure can lead to stress, guilt, or even conflict within the household. Some consider using credit cards to cover the cost, only to face high-interest debt later. Others dip into emergency savings meant for unexpected medical bills or car repairs, leaving the family vulnerable. The fear of saying “no” to an enriching opportunity can weigh heavily, especially when peers are participating. This emotional burden is real—and it’s why relying solely on passive saving is no longer a sustainable strategy for many families.

Shifting Mindset: From Saving to Strategic Investing

The turning point in my own journey came when I stopped seeing the study tour as a sudden expense and started treating it as a planned financial goal. This shift in mindset—from reactive saving to proactive investing—changed everything. Instead of scrambling to gather funds a few months before departure, I began looking at the timeline: my child was in middle school, and the tour would happen in two years. That gave me 24 months to prepare. With that time horizon, I realized I didn’t just have to save—I could grow the money.

The core idea is simple: money left idle loses value over time, but money put to work can grow. Even modest returns, when compounded consistently, can make a meaningful difference. For example, saving $150 per month in a regular account with 1% interest would yield about $3,640 after two years. But investing that same amount in a vehicle earning 4% annually could grow to around $3,760—an extra $120 without increasing monthly contributions. Over longer periods, the gap widens. For a five-year goal, the difference could be over $500. These gains aren’t life-changing on their own, but they cover real costs: airfare upgrades, extra excursions, or even part of a sibling’s future trip.

This approach also forces a healthy conversation about financial priorities. Every dollar allocated to one goal is a dollar not available for another. I had to make choices—delaying a family vacation, cutting back on dining out, or postponing a home renovation. These weren’t sacrifices in the negative sense, but conscious decisions aligned with what mattered most. It became clear that funding my child’s education experience wasn’t just a one-time expense; it was an investment in their confidence, independence, and global awareness. By reframing the cost this way, the effort felt worthwhile, not burdensome.

Opportunity cost—the value of what you give up when making a choice—became a guiding principle. Choosing to fund a study tour through disciplined investing meant avoiding the hidden costs of debt, such as interest payments and stress. It also meant preserving emergency funds for true emergencies. This long-term perspective helped me stay focused, even when short-term temptations arose. The mindset shift wasn’t about becoming a financial expert overnight; it was about making intentional, forward-looking decisions that supported my family’s values and goals.

Investment Tools That Actually Work for Education Goals

One of the biggest barriers to starting is confusion about where to put the money. Many parents assume investing means risky stock market gambles or complex financial products. But for education funding, the goal isn’t high returns at all costs—it’s steady, reliable growth with minimal risk to the principal. The good news is that several accessible, low-to-moderate risk tools can help achieve this without requiring deep financial knowledge.

High-yield savings accounts are an excellent starting point. Unlike traditional savings accounts that offer near-zero interest, high-yield versions—often provided by online banks—can pay 3% to 5% annual percentage yield (APY), depending on the economic environment. These accounts are typically FDIC-insured (in the U.S.) or protected under similar government schemes elsewhere, meaning your money is safe up to a certain limit. The main advantage is liquidity: you can access funds at any time without penalties. This makes them ideal for goals within one to two years. While returns aren’t spectacular, they significantly outpace inflation and standard savings rates, making them a smart upgrade for conservative investors.

Fixed-term deposits, also known as certificates of deposit (CDs) in some countries, offer another layer of growth. With these, you agree to leave a lump sum in the bank for a set period—ranging from three months to five years—in exchange for a higher, fixed interest rate. For example, a 12-month CD might offer 4.5% APY compared to 3.5% for a standard savings account. The trade-off is limited access: withdrawing early usually incurs a penalty. But if you know your child’s tour is 18 months away, a 12- or 18-month CD can lock in a better rate while keeping your money secure. Laddering multiple CDs—spreading funds across different maturity dates—can balance growth and flexibility.

For goals further out—three years or more—diversified bond funds offer slightly higher potential returns with controlled risk. These funds pool money from many investors to buy a variety of government and corporate bonds. Because they are diversified, they are less volatile than individual stocks. While bond values can fluctuate slightly with interest rate changes, high-quality bond funds tend to deliver steady income and modest capital appreciation over time. They are not FDIC-insured, but when held for the long term, they have historically provided better returns than savings accounts with acceptable risk levels. For parents comfortable with a small amount of market exposure, these funds can be a valuable part of a balanced strategy.

Building a Timeline-Based Investment Plan

Timing is one of the most powerful tools in financial planning. The closer you get to needing the money, the more important safety and liquidity become. The further out the goal, the more room you have to accept mild fluctuations for the sake of better returns. A timeline-based approach ensures your money works hard when it can—and stays protected when it must.

Let’s say your child’s study tour is two years away. In the first year, you might allocate funds to a mix of high-yield savings and short-term bond funds. This allows for growth while maintaining access. As the departure date approaches, you gradually shift more into high-yield savings or fixed-term deposits. This “de-risking” strategy ensures that by the time you need the money, it’s in safe, liquid accounts, unaffected by short-term market movements. For example, if the tour is in 18 months, you might buy a 12-month CD six months into the plan, followed by a six-month CD a year later. This way, both mature just in time, and you earn higher interest without locking money away too early.

For longer timelines—say, four to five years—you can afford to be slightly more aggressive in the early stages. A portion of monthly contributions might go into a diversified bond fund or a balanced mutual fund with a mix of bonds and blue-chip stocks. These instruments carry modest risk but offer the benefit of compounding over time. As the goal nears, you systematically move those funds into safer vehicles. This phased approach, known as a “glide path,” is commonly used in retirement planning but works equally well for education funding.

Creating a personalized timeline starts with a clear date: when will the tour happen? Then, estimate the total cost and divide it by the number of months until departure. This gives you a monthly target. From there, match your investment choices to the timeline. If you’re 36 months out, you might start with 70% in bond funds and 30% in high-yield savings. At 24 months, shift to 50-50. At 12 months, move to 80% in savings and 20% in short-term CDs. This structured method removes guesswork and emotional decision-making, keeping you on track without constant monitoring.

Risk Control: Protecting Your Education Fund

No investment is entirely risk-free, but the goal here isn’t wealth creation—it’s reliable funding for a specific purpose. That means capital protection must be the top priority. The biggest threat isn’t market volatility alone; it’s making emotional decisions during downturns. For example, if a bond fund dips 3% in value six months before the tour, panic-selling locks in the loss. Staying the course, however, usually allows recovery, especially if the fund holds high-quality assets.

Diversification, even on a small scale, is a powerful defense. Instead of putting all your education fund into one account or product, spread it across two or three vehicles. This reduces exposure to any single risk. For instance, keeping part in a high-yield savings account, part in a short-term CD, and part in a bond fund creates a balanced portfolio that can withstand minor fluctuations. You don’t need thousands of dollars to diversify—consistent allocation matters more than size.

Another critical risk to avoid is the lure of high-return promises. Scams and speculative products often target well-meaning parents looking for quick fixes. Anything advertising “doubled returns in six months” or “guaranteed 10% gains” should be treated with extreme caution. Real, sustainable growth is gradual. Legitimate financial institutions do not promise unrealistic returns. Always research the provider, check for regulatory oversight, and read the fine print. If it sounds too good to be true, it almost certainly is.

Discipline is the ultimate safeguard. Set up automatic transfers from your checking account to your investment vehicles each payday. This removes the temptation to skip a month or redirect funds to less important expenses. Review your progress quarterly, but avoid checking balances daily—this can lead to overreaction. Remember, the purpose of this fund is not to get rich, but to ensure your child can go on that life-changing trip without financial strain. Keeping that vision front and center helps maintain focus and resilience.

Practical Tips to Stay on Track Without Overcomplicating

Success in funding a study tour doesn’t come from complex strategies—it comes from consistency. The most effective plans are simple, repeatable, and easy to maintain. One of the best tools available is automation. Setting up automatic monthly transfers to your chosen investment accounts ensures that saving happens before you even have a chance to spend the money. Treat it like a non-negotiable bill, just like rent or utilities. Over time, this small habit builds momentum and reduces the mental load of managing money.

Regular progress checks are equally important. Every three months, review your balance and compare it to your target. Are you on track? Ahead? Behind? If you’re falling short, look for small adjustments—cutting one subscription, cooking at home more often, or selling unused items. These micro-corrections keep the plan realistic and adaptable. If you’re ahead, consider whether you want to increase contributions for future goals or allow some flexibility in the budget. The key is to stay engaged without becoming obsessive.

Involving your child in the process can also be powerful. While they don’t need to know every detail, sharing the goal—“We’re saving so you can go on your study tour”—teaches financial responsibility and builds anticipation. Some parents give teens a small role, like tracking progress on a chart or suggesting ways to save as a family. This turns financial planning into a shared mission, not a hidden burden. It also helps children appreciate the value of experiences over material things.

Simple record-keeping goes a long way. A spreadsheet or a notebook with dates, amounts, and account types can serve as a clear roadmap. You don’t need fancy software—just enough structure to see progress. Avoid the trap of chasing trends or switching strategies every time you hear about a “hot” investment. Stability and patience yield better results than frequent changes. Lastly, celebrate milestones. When you reach 25%, 50%, or 75% of your goal, acknowledge it. These moments of recognition reinforce positive behavior and keep motivation high.

Turning Financial Planning Into a Family Win

Funding a study tour through smart investing is about more than just covering a cost—it’s about building confidence, resilience, and shared purpose. When the day finally arrives and your child boards the plane, the pride you feel is not only for their adventure but for the journey you took together to make it possible. That sense of accomplishment doesn’t fade; it becomes part of your family’s story.

The benefits extend beyond the trip itself. You’ve modeled responsible financial behavior, showing that big goals are achievable with planning and patience. You’ve protected your family’s stability by avoiding debt and preserving emergency funds. And you’ve given your child an implicit lesson in delayed gratification—a skill that will serve them well in life. The discipline you practiced doesn’t end with the tour; it sets a precedent for how your family approaches future goals, whether it’s college, home ownership, or retirement.

Most importantly, you’ve transformed financial stress into peace of mind. There’s no last-minute scramble, no guilt over spending, no fear of falling behind. Instead, there’s clarity, control, and the quiet satisfaction of knowing you did it the right way. This isn’t about perfection—it’s about progress. Every family’s situation is different, but the principles remain the same: start early, invest wisely, protect your capital, and stay consistent.

So if you’re standing where I once stood—wondering how to afford an enriching experience for your child—know that you have more power than you think. You don’t need a windfall or a miracle. You just need a plan, a few practical tools, and the willingness to start. The journey of a thousand miles begins with a single step. And in this case, that step leads not just to a destination abroad, but to a stronger, more confident version of your family at home.